News and Announcements

Wholesale Investor Marketing Regulations in Australia

- Published March 27, 2026 5:28AM UTC

- Publisher Wholesale Investor

- Categories Capital Insights, Capital Raising Tips, Trending

Marketing investment opportunities to wholesale investors in Australia is subject to a distinct regulatory framework that differs significantly from retail financial product marketing. While the Section 708 exemptions remove the requirement for a prospectus, they do not eliminate all regulatory obligations. Companies that misunderstand these boundaries risk ASIC enforcement, investor claims, and reputational damage.

This guide explains what you can and cannot do when marketing to wholesale investors, covering the advertising restrictions, anti-hawking provisions, and practical compliance considerations.

The Distinction Between Offers and Marketing

A critical concept in wholesale investor marketing is the distinction between making an offer of securities and providing general information about a company or investment opportunity.

An offer of securities is a specific proposal that, if accepted, would create a binding obligation to issue or transfer securities. Offers made under s708 exemptions must be personal offers directed to individuals.

General marketing, such as brand awareness, thought leadership, educational content, and company profiling, does not constitute an offer of securities. Companies can build their profile and generate interest through content marketing, speaking at events, and media engagement without triggering disclosure obligations, provided the communications do not contain specific offer terms that could constitute a securities offer.

The line between marketing and offering is not always clear-cut, and companies should seek legal advice when structuring campaigns that sit near this boundary.

Anti-Hawking Provisions

Section 992A of the Corporations Act prohibits the making of unsolicited offers of financial products in the course of, or because of, unsolicited real-time contact. In practical terms, this means you cannot cold call or cold message a person to offer them securities unless specific exemptions apply.

The anti-hawking provisions apply regardless of whether the investor is wholesale or retail. The key exemptions include: the person has previously indicated interest in receiving such offers; the person has an existing relationship with the offeror; or the contact is made by a licensed financial services provider in the ordinary course of their business.

For companies raising capital, this means your outreach should be directed to investors who have opted in to receive deal flow, have an existing relationship with your company or your intermediary, or have been introduced through a licensed adviser.

Advertising Restrictions

The advertising restrictions under the Corporations Act apply specifically to offers that rely on the personal offer exemptions. If you are raising under the small-scale offering exemption (20/12 rule), your offers must be personal and targeted. Broad advertising, including social media posts, email blasts to un audiences, and public webinar invitations that include offer terms, can invalidate the personal offer exemption.

Companies using the sophisticated or professional investor exemptions have more flexibility, as these exemptions do not require personal offers. However, any advertising must still comply with the misleading and deceptive conduct provisions, and care must be taken to ensure that communications do not constitute offers to persons who do not meet the relevant thresholds.

A practical approach is to separate your marketing into two layers: public-facing content that builds awareness and educates the market (no offer terms, no specific investment details), and private, targeted communications to verified wholesale investors that contain the specific terms of the offer.

ASIC’s Position

ASIC has historically focused its enforcement activity on cases where companies have used wholesale investor exemptions to effectively conduct retail fundraising, reaching investors who do not genuinely meet the thresholds or using public channels to make what are functionally public offers.

ASIC has also expressed concern about the use of an accountant’s certificates to circumvent disclosure protections, particularly where trust or company structures are used to artificially meet the net asset or income thresholds. Companies should ensure that their investor verification processes are genuine and that certificates reflect the true financial position of the investor.

Compliant Marketing Strategies

Private Capital Marketplaces

Platforms like Wholesale Investor provide a compliant channel for reaching verified wholesale investors. Because investors on the platform have been profiled and verified, communications through the platform are directed to recipients and sit within the regulatory framework.

Advisor and Intermediary Referrals

Working through licensed advisors and intermediaries provides both compliance comfort and commercial effectiveness. Advisors can introduce opportunities to their client base under their own licensing obligations.

Events and Information Sessions

Hosting private events for verified wholesale investors is an effective and compliant approach. Ensure that attendance is restricted to investors and that any offer-related content is delivered in a controlled, private setting rather than broadcast publicly.

Content Marketing

Educational content, thought leadership, industry analysis, and company updates that do not contain specific offer terms can be distributed publicly. This builds brand awareness and drives inbound interest from investors who then engage through compliant private channels.

Trending

Wholesale Investor Marketing Regulations in Australia

Marketing investment opportunities to wholesale investors in Australia is subject to a distinct regulatory framework that differs significantly from retail financial product marketing. While the Section 708 exemptions remove the requirement for a prospectus, they do not eliminate all regulatory obligations. Companies that misunderstand these boundaries risk ASIC enforcement, investor claims, and reputational damage. This […]

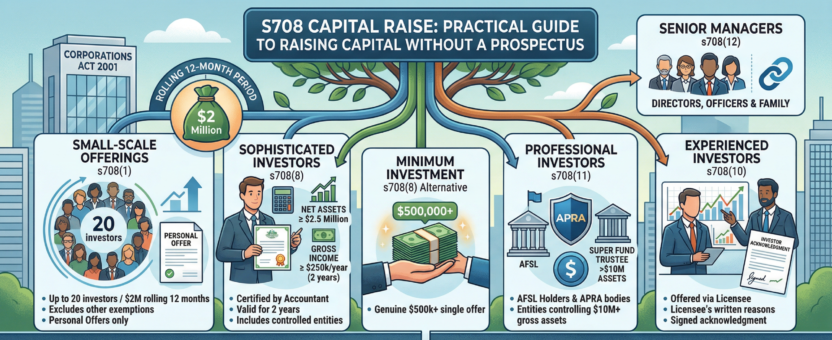

S708 Capital Raise: A Practical Guide to Raising Capital Without a Prospectus

Section 708 of the Corporations Act 2001 is the regulatory foundation for private capital raising in Australia. It defines the circumstances under which a company can offer securities without preparing and lodging a disclosure document such as a prospectus. For founders and fund managers, understanding s708 is not optional. It is the legal framework that […]

Jevons Paradox: The 160-Year-Old Idea That Explains Why AI Is Creating More Jobs, Not Fewer

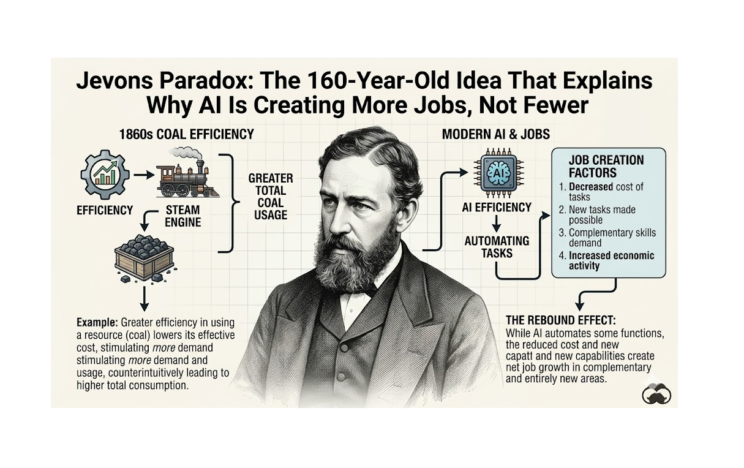

When technological efficiency increases the supply of a resource, it paradoxically leads to higher total consumption and expansion of the market. This pattern, known as Jevons Paradox, played out with steam engines, automobiles, and aviation. Today, the same dynamic is happening with artificial intelligence: AI is making software development cheaper and faster, which is unlocking massive, latent demand for new applications and creating a boom in software engineering roles globally. The key question is what new forms of human effort will emerge when the cost of the old ones drops to near zero.