SYDNEY, NSW — A stark warning has been delivered to Canberra from the front lines of the Australian private funding market. Newly aggregated survey data from 260 of the nation’s founders and sophisticated investors reveal that proposed federal tax overhauls are triggering an immediate, aggressive chill across the nation’s innovation economy.

The findings, published by one of Australia’s largest private marketplace operators Wholesale Investor / CapitalHQ, in a formal submission to the Senate Economics Legislation Committee, suggest that what was originally framed as a targeted housing affordability policy is inadvertently choking the supply of risk capital to productive enterprise.

The Core Friction: CGT and Portfolio Asymmetry

The primary driver of the panic is the proposed replacement of the long-standing 50% Capital Gains Tax (CGT) discount with an inflation-indexed model, working in tandem with a strict 30% minimum tax floor.

For high-net-worth individuals, angel syndicates, and family offices, early-stage investing relies on a power-law dynamic: accepting a high volume of complete losses in exchange for a few outsized “winners.” Sophisticated investors note that taxing indexed gains on a successful venture without a symmetric, balanced recognition of real losses across the broader portfolio fundamentally breaks the math of venture capital. In several analysed models, respondents warned that this imbalance could push the real effective tax rate on an overall portfolio to well over 100%.

Furthermore, the immediate closure of the Eligible Venture Capital Investor (EVCI) program on budget night has isolated the “first money in”. While institutional VC fund structures (VCLPs and ESVCLPs) received threshold increases, deal-by-deal angel syndicates, private individuals, and employees holding Employee Share Ownership Plans (ESOPs) are completely excluded from concessional treatment.

“Risk capital is mobile and will be allocated to the best opportunities in the most welcoming jurisdiction,” one investor respondent noted bluntly. “By implementing the proposed CGT changes, you risk decimating this ecosystem in 18 months.”

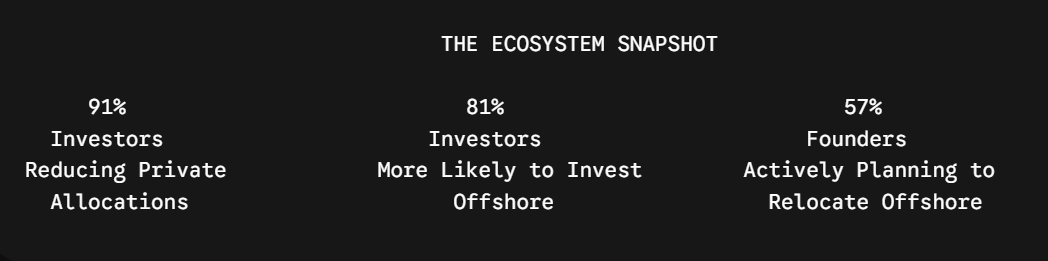

Capital and Talent Eye the Exit

The data indicates the impact is no longer a hypothetical threat; capital flight is actively underway.

An astonishing 91% of surveyed investors have reported a reduced willingness to back Australian private companies. Based on the initial sample of just 110 investors, an estimated $90 million to $180 million in capital allocation has already been delayed, paused, or explicitly redirected offshore since the budget announcement.

The destinations welcoming this displaced wealth and talent are clear: New Zealand, Singapore, the United States, the United Kingdom, and the UAE are repeatedly named as more competitive, predictable jurisdictions.

For founders, the domestic landscape is growing increasingly untenable. 71% of company executives say policy uncertainty has already distorted their operational decisions. More alarming still, 57% of growth-stage founders are currently in active discussions or planning to transition their operations entirely offshore.

Navigating the 10-Year R&D “Cliff”

The Senate submission also highlights deep anxiety in long-development sectors like deep tech, medtech, and life sciences. The proposed legislation threatens to introduce a strict 10-year operating-life cap on refundable Research and Development (R&D) tax support.

Because bringing a complex clinical therapy or advanced hardware asset to market routinely takes 12 to 15 years, the most capital-intensive trial and development years fall squarely after the decade mark. 89% of investors report a severely diminished appetite for funding these sectors if the cap is implemented, threatening to strangle Australian intellectual property just as it approaches global commercial viability.

Recommended Adjustments to Safeguard Innovation

In its submission to the Senate Committee, Wholesale Investor emphasised that the innovation ecosystem broadly recognises the need for housing tax reform. However, to prevent unintended economic self-harm to productive sectors, the group tabled several critical structural recommendations:

- Confine the Scope: Restrict the removal of the 50% CGT discount and the 30% minimum floor explicitly to residential property, preserving the existing settings for innovation company equity.

- Support the Whole Funding Chain: Extend any retained concessional CGT treatments beyond registered funds to encompass individual angel investors, private syndicates, and ESOP holders.

- Restore Loss Symmetry: Reconsider the execution of the 30% minimum tax floor to accommodate lumpy, once-in-a-cycle capital realisations, and allow for equivalent treatment of real losses against gains.

- Protect Deep Tech Cycles: Exempt or significantly extend the 10-year operating cap on refundable R&D incentives for high-capital, long-development sectors like biotech and advanced manufacturing.

As the Senate Committee prepares to review these on-the-ground insights, the message from Australia’s wealth creators is clear: capital will always flow down the path of least resistance. If Australia raises the regulatory barriers to risk-taking, the nation risks losing a generation of innovative companies and the future tax revenues they would have generated.