Australia’s startup ecosystem opened 2026 with a number that demanded attention.

In the first three months of the year, $1.8 billion was raised across 81 venture deals and 26 accelerator rounds. That makes Q1 2026 the strongest start to a year since the 2022 boom, up 63% on Q1 2025, and more than double the same period in both 2024 and 2023.

On the surface, it looks like a full-throated recovery.

Look a little deeper, and a more complicated, and arguably more interesting, picture emerges.

The Australian venture market in Q1 2026 was not a rising tide lifting all boats. It was a series of very large waves breaking on a very specific stretch of beach, while much of the coastline remained calm. Capital is flowing. But it is flowing with a selectivity and concentration that sets this moment apart from any previous recovery.

To understand what’s really happening, you have to look past the headline and into the structure of the quarter: who got funded, what they’re building, why investors paid what they paid, and what it all says about where Australian VC is heading.

The Number Nobody Puts in the Press Release

Here is the statistic that didn’t make the announcements: the top 10 deals in Q1 2026 captured 59% of all capital raised. The top 20 captured 79%.

By the measure of funding concentration, this was the most lopsided quarter in more than seven years.

That context matters enormously for how founders and investors should interpret the $1.8 billion headline. The money was raised. The rounds were real. But the distribution tells a story of a market splitting in two:

- A small number of companies raising transformative, category-defining rounds

- A much larger group of earlier-stage startups finding the market considerably tighter than the aggregate data implies

Sub-$5 million deal activity, historically the lifeblood of the early-stage ecosystem, hit its lowest quarterly level since 2020. Part of the reason is structural: Seed rounds are simply getting bigger, with more than half of Q1 Seed deals coming in above $5 million. But the lived experience of the average early-stage founder in Q1 bore little resemblance to what the headline suggested.

Investors were candid about the disconnect in the Cut Through Quarterly Sentiment Survey:

“The market is in a strange place right now. We’re seeing strong top-of-funnel activity, but deals are moving slowly and I assume many startups are finding it hard to close the deal they set out to.” — Investor, CTQ Investor Sentiment Survey, March 2026

Market sentiment declined from Q1 2025. Fewer investors rated conditions as highly favourable. More settled into a posture of cautious, selective deployment.

The lesson for founders: the headline number is not your benchmark. The relevant question is whether you’re the kind of company that would make the top 20, and if not, what it would take to get there.

AI Has Stopped Being a Category. It’s Now a Valuation Filter.

If there is one theme cutting across every dimension of Q1 2026, deal activity, valuations, investor excitement, sector allocation, it is artificial intelligence.

Not as a standalone segment. As a lens through which the entire market is now being evaluated.

The numbers make this concrete:

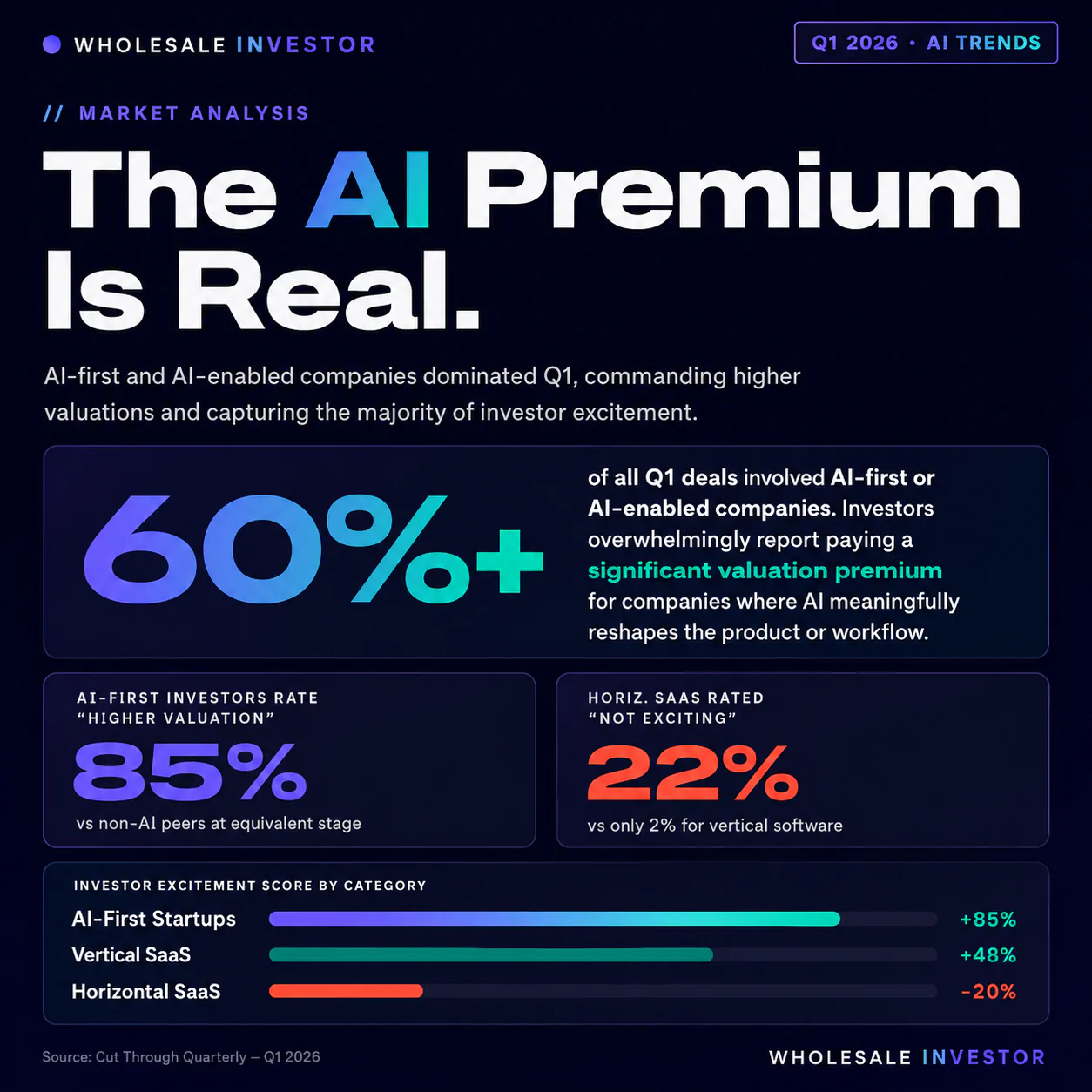

- AI-first and AI-enabled companies accounted for more than 60% of all Q1 deals by count

- The AI-enabled category alone attracted 42% of all venture dollars in the quarter

- For companies founded in the last two years, the absence of AI in the product stack was described as genuinely rare

- Investors overwhelmingly reported AI-first startups commanding higher valuations than non-AI peers at comparable stages

The AI premium is real. But it is not inflating the whole market. It is being concentrated in companies where AI genuinely reshapes the product, the economics, or the customer workflow, not companies where it has been bolted on as a feature.

That distinction is becoming the central judgment call separating strong venture investors from poor ones right now.

As Chris Gillings, founder of Cut Through Venture, wrote in the Q1 report:

“Customers won’t pay for jaw-droppingly magical looking demos. They will pay for AI that solves painful problems, reshapes workflows, improves economics, and builds products they cannot easily walk away from.”

The Losers in an AI-First Market

The flip side of AI’s rise is the pressure it is placing on software categories that lack structural defences to resist it.

Horizontal SaaS, the category-agnostic productivity tools that dominated venture portfolios a decade ago, is in serious trouble. One investor in the survey called it the “SaaSpocalypse.”

The data backs the drama:

| Category | Investor “Not Exciting” Rating | Capital Raised Q1 |

|---|---|---|

| Horizontal SaaS | 22% | $202M (19 deals) |

| Vertical SaaS | 2% | $800M (59 deals) |

The logic is straightforward. AI is compressing development cycles, commoditising feature sets, and lowering barriers to entry in markets where the incumbent advantage was always thin. A horizontal tool that coordinates work or records activity “sits lightly on top of a process”, and that lightness is now a liability.

Vertical software, by contrast, benefits from deep workflow integration, domain-specific data, industry-specific distribution, and switching costs that AI alone cannot dissolve.

This gap is not a temporary valuation divergence. It looks increasingly like a structural realignment.

The Atoms Revolution: Australia’s New Unicorns Aren’t Building Software

Perhaps the most symbolically significant development of Q1 2026 was categorical, not numerical.

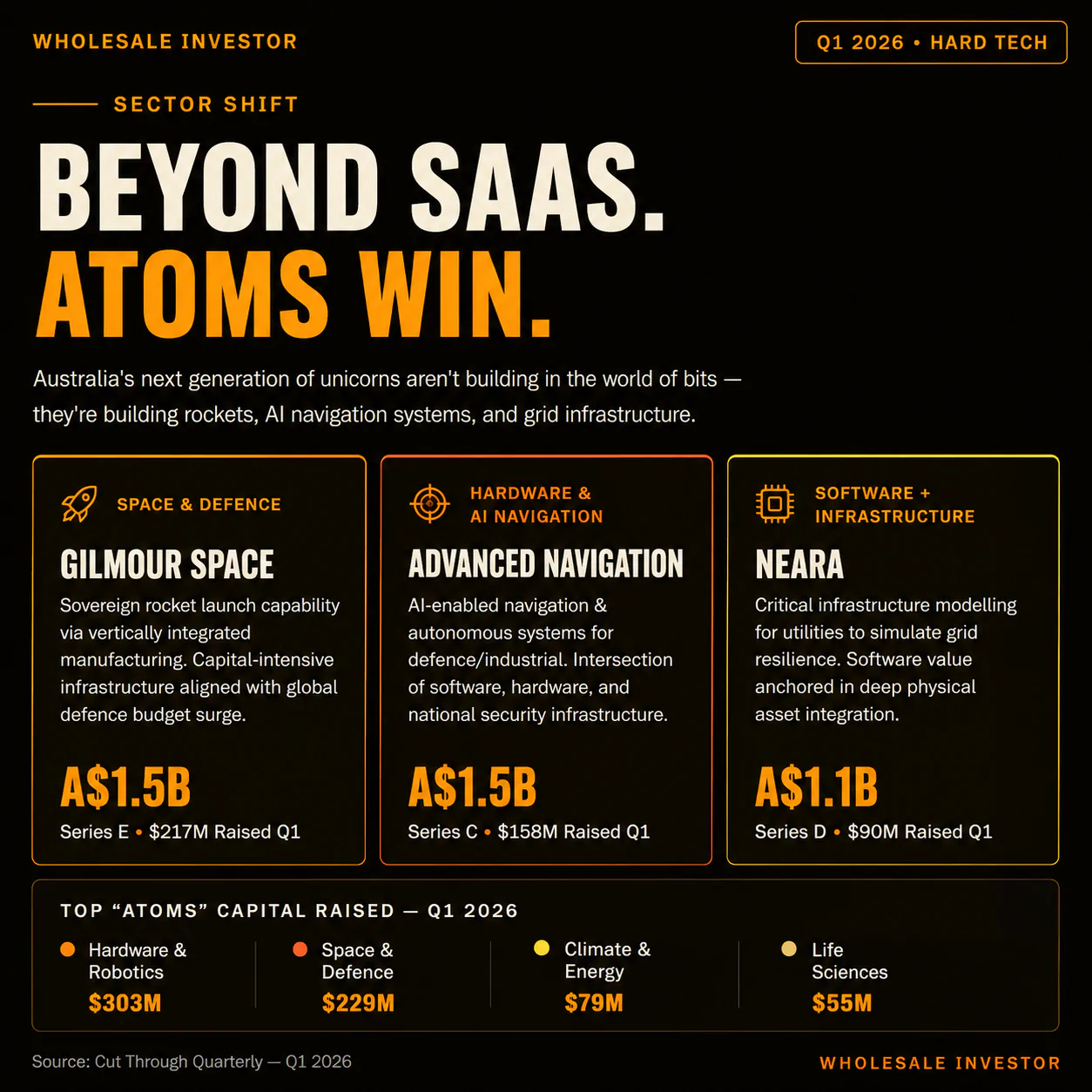

For the first time in recent memory, all three companies that achieved unicorn status in a single Australian quarter were not SaaS businesses.

They were a rocket company, an AI navigation hardware manufacturer, and a critical infrastructure modelling platform. Here’s what they raised:

🚀 Gilmour Space — A$1.5B Valuation

$217M Series E. Developing sovereign launch capability through vertically integrated rocket manufacturing. Capital-intensive, infrastructure-led, and directly aligned with a global surge in defence budgets and strategic autonomy investment.

🤖 Advanced Navigation — A$1.5B Valuation

$158M Series C. Builds AI-enabled navigation and autonomous systems for defence and industrial applications. Sits at the intersection of software, hardware, and national security infrastructure — attracting capital that few Australian companies have seen before.

⚡ Neara — A$1.1B Valuation

$90M Series D. Provides critical infrastructure modelling used by utilities to simulate and manage grid resilience. Software-led, but deeply embedded in physical assets in ways that make it genuinely difficult to displace.

What This Signals

These three companies share a common thread: they are all building in the world of atoms rather than bits.

Long development timelines. Deep integration with regulated physical systems. Value propositions that a well-prompted language model cannot replicate overnight.

The prior generation of Australian unicorns — Canva, Airwallex, SafetyCulture, Deputy — scaled through software distribution and capital efficiency. Their success built an ecosystem optimised for that playbook.

The emergence of defence, space, hardware, and climate infrastructure as dominant themes in 2026’s biggest rounds represents a genuine structural shift. One that will require investors, advisors, and ecosystem infrastructure to develop new capabilities from scratch.

The Sector-Level Data

The scale of capital flowing into “atoms” categories in Q1:

- Hardware, robotics & sensors: $303M across 17 deals

- Space & defence: $229M across 3 deals (average deal: $76M)

- Cybersecurity: $125M, led by UpGuard’s $105M Series C

- AI infrastructure: $100M from Firmus’s strategic round

Five years ago, these sectors barely registered in Australian VC portfolios. In Q1 2026, they accounted for the plurality of capital deployed.

What Investors Actually Want Right Now

The sentiment survey is unusually direct about where conviction sits, and where it doesn’t.

Most excited (net positive score):

- Vertical business software: +48%

- Hardware, robotics & sensors: +45%

- Healthtech: +27%

- AI models & data infrastructure: +23%

Least excited (net negative score):

- Consumer brands: –53%

- Crypto & Web3: –48%

- Consumer tech: –27%

- Horizontal SaaS: –20%

The pattern is consistent. Investors want vertical depth, workflow ownership, AI integration, and physical-world defensibility. They are cool on consumer, broadly sceptical of crypto, and actively worried about horizontal software’s pricing power in an AI-saturated environment.

For founders, the signal is clear. The question is no longer whether AI is in your product, for most new companies, it is, or will be. The question is whether your AI integration creates genuine defensibility: proprietary data, deep workflow ownership, regulatory integration, or physical embeddedness that makes your position durable rather than just impressive in a demo.

For investors, the harder task is resisting the temptation to mistake activity for quality. As one survey respondent put it:

“The question is not whether AI lets you move faster, because it almost certainly does. The question is whether it improves your judgement, your product and your economics — or simply helps you make mistakes at greater speed.”

The Bottom Line

Q1 2026 was an extraordinary quarter by the numbers. Whether it marks the beginning of a sustained, broad-based recovery or another concentrated spike driven by a handful of exceptional rounds is something the data cannot yet tell us.

What it can tell us is this: the Australian venture market is becoming more sophisticated, more selective, and more globally integrated than at any point in its history.

The companies best positioned to benefit are those that have earned their right to capital through genuine depth, not merely by participating in the right theme at the right time.

Key Takeaways

- $1.8B raised in Q1 2026, up 63% year-on-year, but the top 20 deals captured 79% of all capital

- AI-first and AI-enabled companies account for 60%+ of deals and command clear valuation premiums

- Australia’s three new unicorns (Gilmour Space, Advanced Navigation, Neara) are all physical-world companies, a major departure from the SaaS-dominant prior generation

- Vertical SaaS remains the most active deal category; horizontal SaaS faces structural investor scepticism

- The market is open, but only for companies that clear an increasingly high bar

Sources: Cut Through Quarterly Q1 2026, Australian Startup Funding Report. Data covers venture and accelerator rounds announced in Q1 2026. All figures in Australian dollars unless otherwise stated.