We asked active investors what they actually want from credit strategies. The answers should change how every fund manager builds their next product.

The Quiet Shift No One Is Talking About

Private credit has quietly become one of the most interesting parts of the capital stack. Capital is flowing in. New managers are launching. Institutional allocators are increasing their weighting.

But beneath headline growth, investor expectations in private credit have shifted more than most people realise. And if you are a fund manager building products without understanding what allocators actually want today, you are flying blind.

We surveyed active private market investors as part of our 2026 Investor Survey to understand what they actually want from credit strategies. Not what the textbooks say. Not what the conference panels assume. What real allocators with real capital are telling us they need.

The results are clear. And they have direct implications for how credit products should be structured, positioned, and sold.

The Data: Investor Expectations Have Split Into Three Distinct Camps

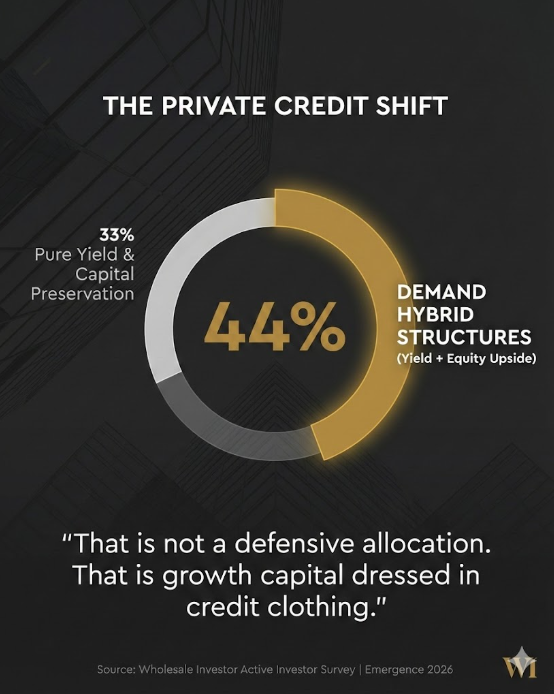

When we asked investors to identify their primary objective for credit strategies, the breakdown was as follows.

33% want pure yield and capital preservation. Senior secured, first mortgage, predictable monthly income. This is a significant portion of the market, and it validates that demand for disciplined, income-focused strategies remains strong. Investors who value capital preservation and reliable distributions are not going anywhere.

But the largest single segment, 44%, now wants hybrid structures that combine yield with equity upside. Mezzanine, venture debt, and structures where income meets optionality.

Another 17% are focused on distressed and opportunistic plays, buying discounted debt for capital appreciation.

The takeaway is not that one approach is right and the others are wrong. It is that the market has diversified. Investors are no longer a monolith. Credit managers who understand which segment they are built to serve, and how to speak to that segment with precision, will outperform those running a one-size-fits-all pitch.

What This Actually Means

The pure yield segment is real, it is substantial, and it is not going away. There will always be a meaningful cohort of investors who need predictable income, capital preservation, and the structural protections that come with senior secured credit. That demand is foundational to the market.

What has changed is that it is no longer the default expectation.

The largest group of credit investors now wants something more. They want income, but they also want optionality. They want structure, but they want upside participation. They are treating private credit not just as a defensive allocation, but as a vehicle that should work harder across more dimensions.

For years, the pitch for private credit was straightforward. Predictable returns. Capital preservation. Low correlation to public markets. Sleep well at night.

That pitch still resonates with a third of the market. And for managers who deliver on it consistently, that is a strong and defensible position.

But the majority now wants something more sophisticated. They want to understand how yield and equity optionality coexist in the same instrument. They want to see how a credit position can participate in upside without sacrificing structural protections.

The Return Expectations Tell the Full Story

When you layer in the return expectations, the picture sharpens further.

42% of credit investors are now targeting 12 to 18% net annual IRR.

That is not a defensive allocation. That is growth capital dressed in credit clothing.

14% are targeting the traditional defensive range of 6 to 8%. Another 30% sit in the balanced 8 to 10% band. But the centre of gravity has moved decisively upward.

The implication is significant. A large portion of investors are willing to accept more risk within credit structures, but they expect to be compensated with meaningful returns and with access to upside. They are not asking for equity risk. They are asking for equity optionality within a credit framework.

What This Means for Fund Managers

If you are a credit fund manager, this data should sharpen how you think about three things.

Product clarity. Know which segment you serve and own it. A pure yield product that delivers consistent, reliable income has a strong market. A hybrid product that clearly articulates how yield and equity optionality coexist has the largest addressable segment. Both are valid. Neither works if you are vague about which one you are building.

How you pitch. Match your narrative to your product and your audience. If you are a pure yield manager, lean into the discipline, the structural protections, and the consistency. If you are building hybrid structures, investors want to hear how your structure captures upside. They want to understand the mechanism, not just the yield. The worst position is somewhere in between, where you are unclear about what you actually offer.

Who are you competing with? Pure yield managers compete with other income strategies across asset classes. Hybrid managers are increasingly competing with equity managers who can articulate a similar risk-adjusted return with a different structure. The lines between credit and equity are blurring, and the managers who understand where they sit on that spectrum will win.

The Bigger Picture

This diversification of credit expectations is part of a broader trend we are tracking across private capital markets. Investors are becoming more sophisticated, more demanding, and more specific about what they want. The days of raising capital with a generic pitch and a well-designed deck are ending.

The data from our 2026 Investor Survey shows this across every category. 75% of investors rank management track record as their top decision factor. 47% are focused on Series A and B opportunities with proven traction. 51% cite lack of liquidity as their primary frustration.

Across the board, investors are telling us the same thing. Give me substance. Give me structure. Give me a reason to believe this is going to work.

Private credit is simply the latest category where that demand for specificity and sophistication is showing up in the numbers.

Where This Conversation Continues

We have built a dedicated high-yield and private credit track into Emergence 2026 specifically because of what this data is telling us.

Fund managers and allocators who are actively shaping this part of the market will be in the room. The conversations will be about product structure, return expectations, and how to build credit vehicles that match what investors actually want, not what the industry assumes they want.

Whether you are a manager delivering disciplined yield or building the next generation of hybrid credit products, this is where the market is headed. And these are the people defining it.