News and Announcements

Why the 20-Year Hold Is the Secret to Australian Life Sciences Returns

- Published March 13, 2026 12:00PM UTC

- Publisher Bella Battsengel

- Categories Capital Insights, Capital Raising Tips, Events, Life Science Hub

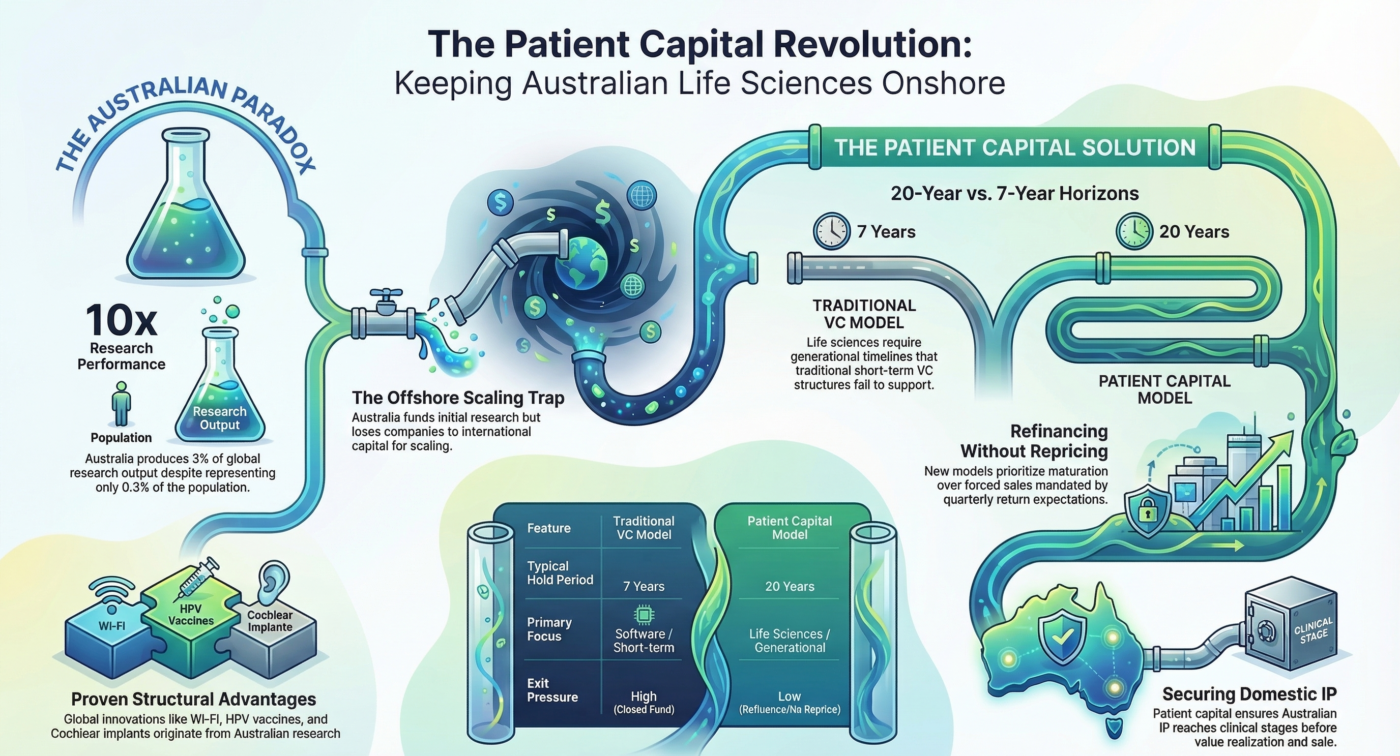

Australia represents 0.3% of the world’s population. Yet it generates more than 3% of global research output.

Cochlear implants. Wi-Fi. The HPV vaccine. These are not statistical anomalies. They are proof points of a structural advantage that Australia has failed to capitalise on.

The country has a world-class research base. But it watches companies scale offshore. The pattern repeats. Fund the initial research. Build early traction. Then lose the company to international capital that understands how to scale life sciences businesses.

This is changing. A new investment model is emerging in Australian life sciences. The 20-year hold.

What Patient Capital Actually Means in Life Sciences

Traditional venture capital operates on seven-year closed fund structures. Two and twenty fee models. Quarterly return expectations. This works for software. It fails catastrophically for life sciences.

Proto Axiom runs a deliberate patient capital structure with 20-year hold periods. They refinance without repricing. They do not sell at 10 years even if the market tells them to.

This is not sentimentality. This is recognising that life sciences operates on generational timelines. That Australian IP deserves infrastructure that matches its development cycle.

The asset going into clinic would not exist without this structure. Traditional VC timelines would have forced a sale before value realisation. Patient capital allowed the science to mature into commercial outcomes.

Why No Australian VCs Were in the AUD$1.5 Billion Medici Deal

Medici Bioventures just closed the largest licensing deal in Australian history. AUD$1.5 billion from UK-based Syncona Bio.

Not a single Australian venture capital firm participated in that deal.

Not because Australian VCs missed the opportunity. Because systemic structural constraints prevent them from investing in certain life sciences models.

This reveals the fundamental problem. Australian capital structures are designed for exits. Life sciences creates value through licensing, partnerships, and long-term platform development. These paths do not align with traditional VC fund economics.

Flagship Pioneering. Roivant Sciences. Syncona Bio. These are the firms that understand platform capability models in life sciences. Roivant was spacked for USD$7.2 billion in seven years by Vivek Ramaswamy. This was not a moonshot. This was savvy platform construction. Licensing deals from pharma tied into a holding company structure.

The familiarity with this business model is very American. Very English. Very European. It has not taken root in APAC.

If the structural opportunities of APAC are to be realised, if the sovereign potential of Australia is to be captured, this infrastructure gap must close.

The Capital Australian Life Sciences Actually Needs

The capital needed is not AUD$5 million into early stage companies today. It is AUD$100 million two years from now. Because that is the asset class life sciences operates in. That is the opportunity.

The ability to think in long-term horizons. To deploy capital without repricing. To build truly interesting companies. More CSLs. A homegrown Thermo Fisher equivalent. That is the opportunity.

But it requires capital structures that align with 10 to 20 year development timelines. Not quarterly return expectations.

How to Assess Life Sciences Without Being a Scientist

Most investors avoid life sciences because they believe scientific expertise is required. This is false.

You do not need to be a deep scientific expert to invest in life sciences. But you do need structure.

Investors are not there to repeat the science. Not there to validate experiments. They are there to assess outcomes.

Science creates the option. Structure creates the outcome and value realisation.

A structured assessment framework looks at:

Biology plausibility. Not is this accurate. Does this make sense. Is it logical. Does the mechanism align with known pathways.

Expert reaction. Bring in key opinion leaders who are experts in that particular pathway or disease indication. Assess their reaction to the technology. Are they excited. Do they see clinical utility. Do they have appropriate scepticism.

Competitive landscape. Who else is playing in this field. What sort of activity surrounds those companies. Are they getting funded. Acquired. Partnering.

Market traction. Has the company had good conversations with big pharma. Those potential buyers of the asset. Are regulatory pathways clear. Are there precedents for approval.

Life sciences has good asymmetry when it comes to returns. But you do not need to get into the weeds to determine whether an investment is worth making. It is probability assessment. Power law dynamics. Having good determination as to whether this has legs to make impact.

The Exact Moment Investors Move From Interested to Committed

For 4D Medical, the pivotal moment was when investors could see a clinical community that understood the value proposition. When they could get face time with doctors who said “4D Medical solves my problems.”

It is easy to get someone excited by technology. Business success comes from solving customer problems. When you can bring customers to investors as a healthcare company, when you can bring doctors who articulate the clinical need, that is when investors get excited.

For Dimerix, the moment was external validation. When they partnered their lead asset DMX-200 with a European company in 2023. External investors could see that another company had turned over the rocks, looked underneath, and still put money down.

That external validation increased liquidity and valuation immediately.

Why Seed Investors in 4D Medical Are Sitting at 38x Returns

The seed investors in 4D Medical are currently sitting at approximately 38 times their money. The company has a market cap of AUD$1.7 billion.

But if those investors had done more work during due diligence, they would have identified more places where the company could have failed. Dozens of risk points. Dozens of potential failure modes.

Most investors do more and more work to identify and zoom in on more risks. They find all the points of failure. But there is also a pathway to success amongst those risks.

Good investors understand the balance between risk and reward. If you get wrapped around only thinking about risk, 2% returns are for you.

Risks can be mitigated. The best mitigating process is people. If putting smart people on the job and working really hard can solve the problems, they will get solved. Not guaranteed. But that is the thesis.

The Credit Card Moment Every Founder Remembers

4D Medical had an investor signed up. The check was delayed. The check did not show up. The founder had just moved his family to the United States. He put payroll on the credit card that month. Next month’s rent went on the credit card.

Difficult conversation with the family. But he believed in the team and the mission. Investors filled the gap.

Dimerix has not yet had to fund the company with a credit card. But as companies get bigger, it gets harder. The key is investors buying into the mission. Understanding that key inflection points are what they are investing in.

For phase three clinical trials with two-year study periods, there will not be news until the outcome comes through. Having alignment between investors on timeframes is critical. Management will do everything humanly possible to deliver on schedule. But noise creates anxiety.

When macroeconomic issues impact programs, when new assets are being evaluated, the key deliverable that allows new capital in or capital out must be clear from the beginning. Investors need to know what they are investing in. They need faith in management to do everything needed until they get there.

Why 4D Medical Keeps 85% of Workforce in Australia

4D Medical has 85% of their workforce in Australia. 90% of their investors are offshore. 97% of their customers are offshore.

This works.

It is easier to leverage the talent pool locally and export the product to the US than to try the inverse. Australia has an incredible talent pool. A world-class healthcare system. A flow of ideas from research that is second to none.

The narrative that Australians do not think big is being challenged. 4D Medical talks a big story to investors. Investors listen. You can trust investors to hear an honestly big story.

The company has grown to a AUD$2 billion market cap. They are absolutely just getting started. They talk about how and why they will get there. Investors follow on that journey.

The CSL Restructure: A Hidden Investment Opportunity

CSL is going through a massive restructure. A lot of people are being let go. This is problematic. But it is also an investment opportunity that the government does not fully realise.

When discussing sovereign capability throughout the supply chain, these people being let go will go to America. Australia’s best talent pool. PhDs with deep expertise. They will follow commercial outcomes most likely. Because there are not enough success stories to catch that windfall domestically.

This is an investment opportunity from both government and private capital perspectives. Australia needs more national champions. The CSL restructure creates a talent pool looking for opportunities. If Australian capital does not capture this, international capital will.

Why Australian Life Sciences Assets Are Undervalued

Right now, Australian life sciences companies have great clinical evidence. Strong data. Promising assets. But they are not valued at what they would be on a global stage.

This discrepancy is the investment opportunity. Artesian identified this with Clarity Pharmaceuticals. They invested early when the company was doing formative fundraising. The company develops a theranostic approach to serious cancers. Both diagnostic and therapeutic capabilities.

Platform applicability. Strong team focused on execution. Capital efficiency in reaching inflection points. These characteristics allowed the company to prove market potential before requiring massive capital.

Australian life sciences opportunities have biology plausibility. Capital efficiency. Stellar scientific expertise. Commercial acumen. There is significant opportunity to capitalise on currently. Helping these companies scale so they reach full potential rather than selling offshore prematurely.

The Infrastructure Gap That Pushes Companies Offshore

Synchron developed brain computer interface technology. The first person implanted was in Australia. They competed against and beat Neuralink in early clinical milestones.

Yet they had to move overseas. Capital constraints. Lack of follow-on funding. Inability to scale domestically.

The National Reconstruction Fund is now funding them to bring manufacturing back. But the pattern reveals the problem. Australia excels at discovery. It hesitates at scale.

This hesitation pushes excelling companies overseas. Not because Australian science is inferior. Because Australian capital infrastructure cannot support companies through long development cycles.

Why do companies leave Australia. Capital has been constrained in life sciences for a long period. It has been a scrap from small inflection point to small inflection point. This is changing. Bigger funding is coming through for earlier stage investments. Multiple VCs now operate in Australia focused on life sciences. Ten years ago, this would not have been possible.

But the combination of management teams with capacity and capability to think big and deliver operationally on large programmes is still lacking. Whether government or industry needs to bring those jobs back, people who can deliver bigger programmes are needed. Australia excels at early inflection points. Building bigger companies requires different infrastructure.

Why Now Is the Right Time to Invest

Historically, capital for life sciences in Australia has been extremely tight. Offshore activity happened because disciplined investors allocated capital responsibly within structural constraints. This is changing.

More specialised capital for life sciences is entering the ecosystem. Allocators are educating their limited partners who previously did not understand the sector. More capital is available. The R&D opportunities coming through universities and research institutes are second to none.

The ecosystem is becoming more savvy about how to make these investments. Great clinical trials infrastructure. Regulatory pathways. A unique window of opportunity exists for investors to invest in life sciences and get uplift on investments before globalisation happens in early stage companies.

There have never been more smart, enthusiastic people with amazing ideas. It has never been easier for them to export outcomes overseas. Right now, companies in Australia have great clinical evidence. Assets are not valued at global stage levels.

That discrepancy is the opportunity.

The 20-year hold is not about refusing to exit. It is about building infrastructure that allows Australian IP to mature into commercial outcomes rather than forcing premature sales. Patient capital creates more CSLs. More national champions. More sovereign capability.

The question is whether Australian capital will build this infrastructure before international capital captures the next generation of breakthroughs.

#PatientCapital #LifeSciencesInvesting #AustralianBiotech #LongTermInvesting #LifeSciencesAustralia #BiotechFunding #20YearHold #SovereignCapability

Life Science Hub

Why the 20-Year Hold Is the Secret to Australian Life Sciences Returns

Australia represents 0.3% of the world’s population. Yet it generates more than 3% of global research output. Cochlear implants. Wi-Fi. The HPV vaccine. These are not statistical anomalies. They are proof points of a structural advantage that Australia has failed to capitalise on. The country has a world-class research base. But it watches companies scale […]

The ‘Unused Billion’: How Points4Purpose is Disrupting the Flatlining Loyalty Market

The loyalty industry is plagued by “sameness,” leaving billions in value dormant. Ivan Schwartz’s Points4Purpose is disrupting this flatlining market by turning rewards into a liquid currency for rent, bills, and over 1.8 million charities.

1,000km, sustainable, efficient , no onboard pilot: How ‘Gap Drone ’ is rewriting the rules of remote logistics

Can autonomous drones solve Australia’s “tyranny of distance”? GAP Drone CEO Liesl Haris thinks so. With the launch of ATLAS—an autonomous transport logistics aircraft system—the company is bypassing traditional infrastructure to deliver 50kg payloads over 1,000km. Dubbed the “Uber of airfreight,” GAP Drone is tackling the “too hard basket” of remote logistics, partnering with Australia Post to provide First Nations communities and regional hubs with reliable, low-cost access to medicine, food, and economic opportunity. By operating within current regulatory frameworks and utilising a “no-runway” launch model, GAP Drone is transforming air freight from an expensive luxury into a scalable utility.